|

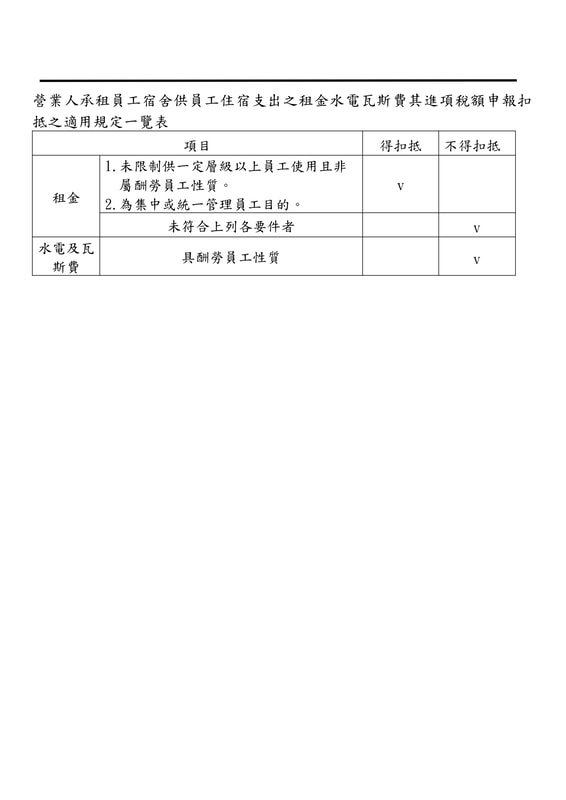

依110年9月9日發布台財稅字第11004590840號令核釋,該承租供總、分支機構員工使用之員工宿舍,符合「未限制供一定層級以上員工使用且非屬酬勞員工性質」(例如未以員工擔任之職位或頭銜限制其使用宿舍權利且不具酬勞性質)及「為集中或統一管理員工目的」(例如由營業人統籌管理宿舍使用規範)等2項要件者,認屬供本業或附屬業務使用,營業人支付租金之進項稅額准予扣抵銷項稅額 至後續發生水電及瓦斯費等支付之進項稅額,考量該等費用係依入住員工使用情形產生多寡差異,具有個別報償性,且與營業人本業或附屬業務無直接關聯,依75年8月4日函規定,不得扣抵銷項稅額。 營業人承租員工宿舍供員工住宿支出之租金水電瓦斯費其進項稅額申報扣抵之適用規定製作一覽表如附件。  |

|

Nexia Trans-Asia Associates is a member firm of the “Nexia International” network. Nexia International Limited does not deliver services in its own name or otherwise. Nexia International Limited and the member firms of the Nexia International network (including those members which trade under a name which includes the word NEXIA) are not part of a worldwide partnership. Nexia International Limited does not accept any responsibility for the commission of any act, or omission to act by, or the liabilities of, any of its members. Each member firm within the Nexia International network is a separate legal entity. |

版權所有 © 2018 Nexia Trans- Asia Associates, CPAs Post All Rights Reserved. |

RSS 訂閱

RSS 訂閱