|

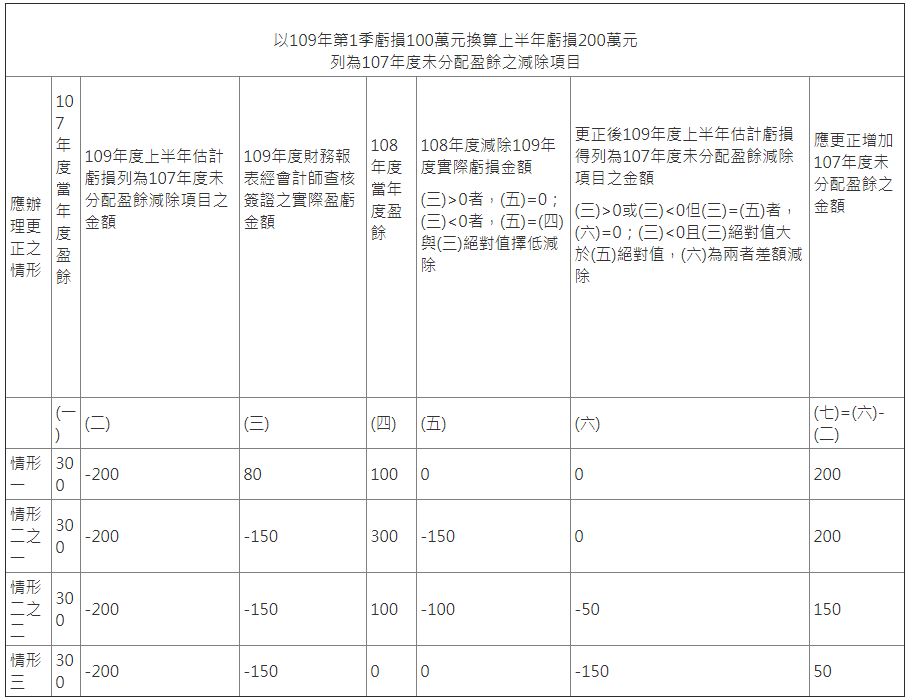

財政部臺北國稅局表示,因應嚴重特殊傳染性肺炎(COVID-19)疫情,財政部於109年5月核釋營利事業經會計師核閱之109年度財務報表第1季虧損,得按該季期間相當半年之比例,換算109年度上半年估計虧損,於申報107年度未分配盈餘應加徵之營利事業所得稅時,依所得稅法第66條之9第2項第8款規定,列為未分配盈餘之減除項目(下稱估計虧損減項)。但其辦理108年度未分配盈餘申報時,應檢視109年度全年度實際盈虧,如有以下說明所列應更正之情形者,應併同辦理更正107年度未分配盈餘申報,調整估計虧損減項數額,並補繳該年度未分配盈餘應加徵之營利事業所得稅: 一、109年度全年度稅後損益為盈餘者。 二、109年度全年度稅後損益為虧損,惟108年度稅後損益為盈餘者,109年度虧損應優先自108年度未分配盈餘減除,減除後無虧損餘額,或該虧損餘額小於107年度未分配盈餘之估計虧損減項者。 三、109年度全年度稅後損益為虧損,108年度全年度稅後損益為零或虧損,惟109年度全年度虧損小於107年度未分配盈餘之估計虧損減項者。 舉例說明如下:  為免營利事業漏未檢視,108年度未分配盈餘申報書增列「表二、以109 年度上半年估計虧損列為 107 年度未分配盈餘減除項目者於本年度檢視結果」以核算是否應更正申報107年度未分配盈餘申報並補繳稅款。

營利事業於辦理108年度未分配盈餘申報時,應確實依109年度全年度實際盈虧,檢視是否應辦理更正107年度未分配盈餘申報,以免遭稽徵機關核定補徵稅款。 資訊來源:財政部新聞稿 https://www.mof.gov.tw/singlehtml/384fb3077bb349ea973e7fc6f13b6974?cntId=93c878bd61c244668c024eee2330ce6c 評論已關閉。

|

|

Nexia Trans-Asia Associates is a member firm of the “Nexia International” network. Nexia International Limited does not deliver services in its own name or otherwise. Nexia International Limited and the member firms of the Nexia International network (including those members which trade under a name which includes the word NEXIA) are not part of a worldwide partnership. Nexia International Limited does not accept any responsibility for the commission of any act, or omission to act by, or the liabilities of, any of its members. Each member firm within the Nexia International network is a separate legal entity. |

版權所有 © 2018 Nexia Trans- Asia Associates, CPAs Post All Rights Reserved. |

RSS 訂閱

RSS 訂閱