|

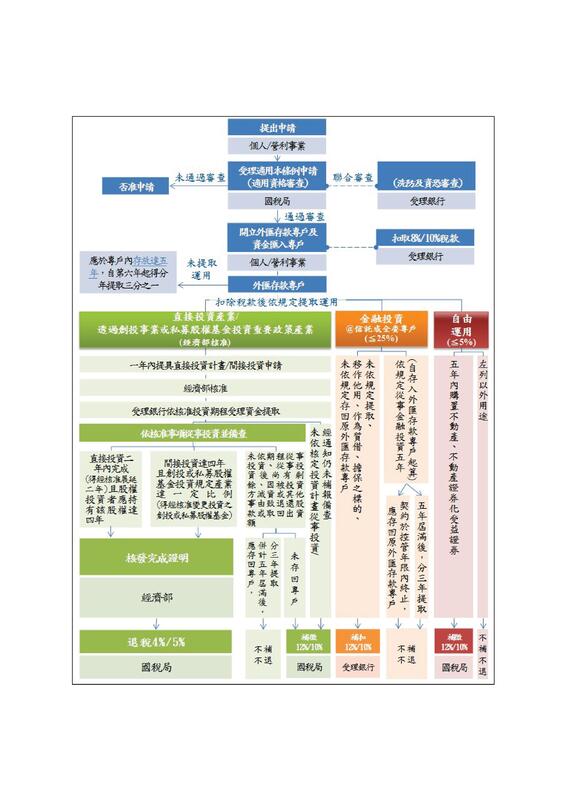

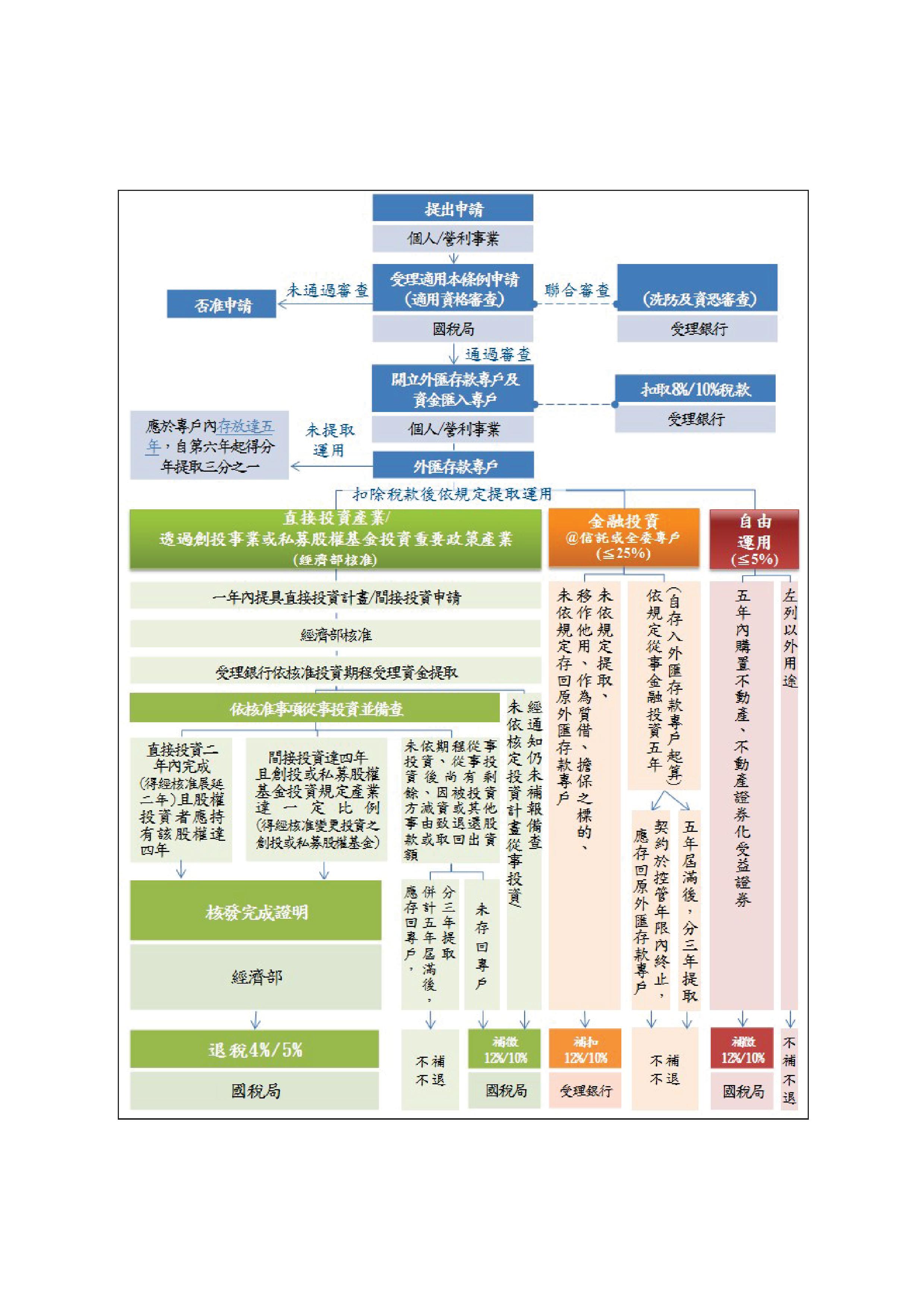

個人匯回境外資金及營利事業匯回境外轉投資收益,得選擇適用「境外資金匯回管理運用及課稅條例」(下稱專法),免依一般所得稅制課稅,但一經擇定不得變更。相關摘要如下: 1.期限:自108年8月15日起施行2年 ,110年8月14日前申請適用 2.受理申請機關(單位): 個人向戶籍所在地國稅局申請;營利事業向登記地國稅局申請。 3.適用範圍: (一) 個人:施行日起算 2 年內匯回境外資金。 (二) 營利事業:施行日起算 2 年內自其具控制能力或重大影響力之境外轉投資事業獲配並匯回之投資收益。 4.申請及後續管理運用:詳流程圖 (JPG檔) (資料來源:國稅局)  評論已關閉。

|

|

Nexia Trans-Asia Associates is a member firm of the “Nexia International” network. Nexia International Limited does not deliver services in its own name or otherwise. Nexia International Limited and the member firms of the Nexia International network (including those members which trade under a name which includes the word NEXIA) are not part of a worldwide partnership. Nexia International Limited does not accept any responsibility for the commission of any act, or omission to act by, or the liabilities of, any of its members. Each member firm within the Nexia International network is a separate legal entity. |

版權所有 © 2018 Nexia Trans- Asia Associates, CPAs Post All Rights Reserved. |

RSS 訂閱

RSS 訂閱

{kind=link}